In-depth analysis of crude oil futures contract pricing and arbitrage strategy analysis

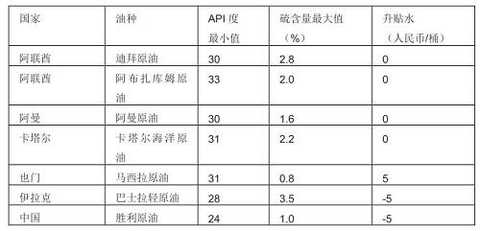

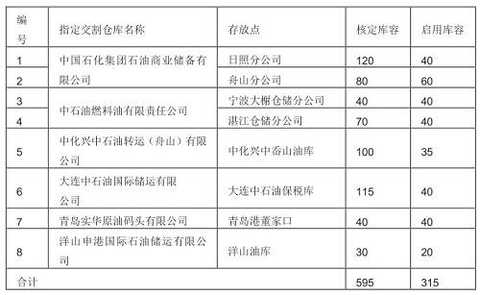

Wen Hao, Long Hao Jian Yue, Zhonghai Petrochemical Import and Export Co., Ltd. Shanghai crude oil futures will be listed on the Shanghai International Energy Exchange Center on March 26, and Shanghai crude oil futures, which have been brewing for many years, have finally landed. For a time, Shanghai crude oil futures became the focus of media hot reviews. Some people think that Shanghai crude oil futures will compete with WTI and Brent crude oil futures, break the Western monopoly of global oil price rules, and help China achieve greater pricing power of crude oil. Some people cheered that Shanghai crude oil futures based on RMB settlement marked "oil renminbi." "The coming of the times. More foreign media reported that China will help the internationalization of the renminbi by achieving full convertibility between oil, renminbi and gold. Although the financial and political significance of Shanghai crude oil futures is rapidly rising, but the high-rise buildings are flat, the castles in the air do not exist. To achieve these long-term financial and political goals, it is still necessary to consolidate the industrial base of Shanghai crude oil futures. The basic framework of contract design, "international platform, net price transaction, bonded delivery, and renminbi pricing" can be said to be a compromise and clever conceiving of many pertinent opinions after repeated discussions. On March 12th, the Energy Trading Center announced that the listing contract began to extend from 1809. The rational pricing range of the contract has become the focus of everyone's attention, combined with the discussion in the early stage of the market, to express personal views and opinions. 1. Shanghai crude oil futures main contract price anchor: the fair value of the main contract In the current international crude oil market system that has matured, the price of Shanghai crude oil futures cannot be born out of thin air. Like a person who first went to the market to sell vegetables, the easiest way to make a vegetable price is to ask for a nearby booth. The balance of supply and demand in the global oil subregion and the geographical attributes of Shanghai crude oil futures and the design of delivery oils have determined that Shanghai crude oil futures prices will currently be anchored through cross-regional arbitrage through cross-regional arbitrage. The anchoring mechanism for the spread between the two regions is not only applicable to Brent and WTI, Brent and Dubai, but also applies to Shanghai crude oil futures. International crude oil futures contracts are listed for trading in the month of delivery. Generally, the monthly contract with the best liquidity (the largest trading volume) is called the main contract. In the WTI, Brent and Oman crude oil futures markets, the main contract is the first line (first line) contract. For example, the first contract month of WTI crude oil futures traded in the first half of March is April, the first contract month of Brent crude oil futures is May, and the first contract month of Oman crude oil futures is May. Every day, the settlement price of the first crude oil futures contract is widely reported by the news media and becomes a well-known international oil price. Table 1 Shanghai crude oil futures deliverable oil grade, quality and premium standards This means that any industrial customer who can participate in futures trading can obtain Oman crude oil at a lower threshold. Other deliverables of Shanghai crude oil futures, such as Dubai, Upper Zakum, Basrah Light crude oil, etc., have higher spot operating thresholds and more complex prices (upgrading fluctuation). Therefore, the most intuitive and fast cross-regional arbitrage channel can be constructed with reference to Oman crude oil. Figure 1 Schematic diagram of price anchoring relationship of Shanghai crude oil futures First, the determination of the main contract month. Shanghai crude oil futures adopt a continuous contract design that is in line with international standards. Under the contract listing month rule, the main contract of Shanghai crude oil futures will not be the first contract. If Shanghai crude oil futures are already in normal operation, according to the rules, the first contract of Shanghai crude oil futures traded in the first half of March is April. Since the delivery oils designed by the Shanghai crude oil futures contract are not based on local resources, but the Middle East medium-grade sulfur-containing crude oils such as Dubai and Oman are the delivery resources, the shipment of Oman crude oil to China in May is basically in June. Master, after the warehouse, the production warehouse receipts can only be delivered to July; therefore, the first contract of Shanghai crude oil futures and the first contract of Oman crude oil futures cannot be synchronized in the arbitrage relationship, which means that the main force of Shanghai crude oil futures It is difficult for a contract to be positioned on the first contract in the early stages and even in the future. If positioned in accordance with Oman crude oil futures, the July contract of Shanghai crude oil futures has a good arbitrage relationship with the May Oman crude oil futures contract. Therefore, with the current month as M month, the first contract month of Brent and Oman crude oil futures is M+2 month, and also the main contract month, the first contract month of Shanghai crude oil futures contract is M+1 month, and the main force The high probability of the contract month will fall in M+4 months. Figure 2 Location of the main contract of Shanghai crude oil futures The main contract month has the best transaction participation value for general customers and non-delivered participants. Price calculations can be carried out and evaluated in real time. From the port of Oman in the Middle East to the domestic delivery warehouse, the main cost components are: the offshore price of Oman crude oil (the first-row crude oil price of DME Oman crude oil + physical delivery cost), and the one-way shipping cost (based on VLCC large tanker). Cargo insurance costs, loss during the first round of shipping (insurance company provides 0.5% deductible rate), port unloading fee, delivery cost (commodity inspection fee + handling fee), storage quota loss (0.06%), delivery warehouse storage fee. FOB cost: Because it is based on real-time star-tapping calculations, Oman crude oil offers do not need to go to the spot physical market for inquiry, mainly to see the first line of DME Oman trading window. Due to the non-main trading hours of Oman crude oil futures (between 4:00 and 4:30 pm in Beijing time), the trading liquidity is not good, so the price difference between buying and selling (buying one price and selling one price) is very large. Obviously, it is not always possible to replace it with a middle price. And this trading period, Shanghai crude oil futures have been closed. Therefore, more professional information is needed to determine the price of Oman. However, if it is a rough assessment, we can calculate the price difference between DME Oman and ICE Brent based on the first settlement price of DME Oman crude oil at 4:30 pm (ICE will announce a minute of 4:30 pm Beijing time). Brent price), and then based on the change in Brent crude oil futures price, the price of DME Oman can be estimated by deducting the 4:30 time spread with the latest Brent crude oil futures price at night. The cost of physical delivery can be determined by the external brokerage company, mainly in the cost of issuing licenses, delivery fees, futures trading fees or brokerage fees. One-way shipping charges. First of all, basically speaking, the loading conditions in the Middle East are better. Each oil type has the oil loading conditions of large VLCC tankers. Therefore, it is recommended to use VLCC large tankers for the shipping cost calculation. The flat rate from the port of Oman to the port of each transfer warehouse can be obtained through a ship broker or computing agency. This parity rate is updated once a year. For example, the rate from Oman loading to Zhanjiang is USD/ton, and the rate to Dalian is USD/ton. Then, the number of tanker WS points is obtained. Since the tanker is generally rented in the Middle East, the current WS points do not represent the actual tanker WS points for M+2 months, and there will be certain errors and risks. However, fortunately, the current supply of the tanker market is oversupply, and the freight rate of the tanker is not volatile. Cargo insurance and short-term deductibles. In general, marine cargo will be insured. The insurance rate can be quoted by the insurance company (especially when the situation is tense, the war risk is high), and the insurance company's short-term deductible rate is five thousandths. That is to say, from the issuance of the bill of lading to the port of loading, to the unloading of the commodity inspection, the intermediate differential insurance company will only provide compensation for more than five thousandths. Therefore, this can be considered as an upper limit. The details are: whether the insurance company is the ship inspection data or the shore tank data of the port of discharge, it needs to be clear, otherwise the odds ratio will be raised to 1%. Port discharge fee. The port unloading costs of various ports actually have many details, such as loading and unloading fees, port and miscellaneous fees, port construction fees, oil pollution fees, security fees and so on. Therefore, the average customer is inclined to sign the overall cost in the form of picking up the package fee. According to the current situation, there are differences in the cost of loading and unloading in various places, and the cost is at the level of 25-35 yuan/ton. Delivery fee. Mainly the warehousing fee, inspection fee and warehousing fee. The delivery fee is paid to the Energy Trading Center, and the standard is 0.05 RMB/barrel. The inspection fee is given in accordance with the standards of the inspection agency (reference price: 0.04 yuan / barrel), currently China Inspection and Certification Group Inspection Co., Ltd., Standards Technical Service Co., Ltd., Shanghai Oriental Tianxiang Inspection Service Co., Ltd., Shanghai Entry-Exit Inspection and Quarantine Bureau The Industrial Products and Raw Materials Inspection Technology Center was approved to be the development and inspection agency for the bonded and delivered business of crude oil futures. The upper limit of storage costs is 0.2 yuan / barrel day. Inbound storage loss. The Shanghai crude oil futures trading rules determined that the warehouse's fixed loss was 0.12%, and the warehousing (seller) and the warehousing (buyer) each took 0.06%. Oman crude oil (Zhanjiang delivery) to the shore into the tank cost calculation table Conversely, if the M+4 Shanghai crude oil futures price is lower than the M+2 Oman crude oil futures CIF price, then China, and even some Asia-Pacific refineries can buy Shanghai crude oil futures delivery instead of purchasing Middle East Oman equivalent. Quality crude oil. Therefore, in terms of the Oman crude oil anchoring model, the first line of contracts should revolve around the tank price fluctuations in Oman. Based on the Middle East is the oil producing area, China is the importing area, and the two areas are in a complementary balance. The Shanghai crude oil futures are more reasonable than the Oman landing price, otherwise the supply will not be enthusiasm. However, due to the global market pattern, the resources of the Western Region have always been eyeing the East, and arbitrage competition has always existed. Therefore, the price difference between Brent and Dubai and the spread between WTI and Dubai will have an impact on the upward operation of the main contract of Shanghai crude oil futures. The lower position runs from demand disturbances in the area, which on the one hand comes from the fluctuations of the industrial refinery and on the other hand from the inventory of trade. Therefore, increasing the regional crude oil inventory reserves is conducive to maintaining the demand side to combat the supply side impact, to avoid excessive fluctuations in oil prices, but this inventory cost will eventually have to pay for the market. On the one hand, the size of the national oil reserve is not enough. On the other hand, the storage capacity of the delivery warehouse can be more. The commercial spot inventory formed by Shanghai crude oil futures will certainly play a role in regulating the short-term supply and demand balance. 2. Shanghai crude oil futures delivery oil "bad money" gold mining: the impact of delivery warehouse and Basra light crude oil If there is a balanced pattern between the Middle East and the Asia-Pacific, then there is a kind of volatility between the Middle East benchmark crude oil and Shanghai crude oil futures. However, the problem lies in the complementary balance model between Asia-Pacific and the Middle East. Under this model, if the scale of demand disturbance in this area cannot be accurately predicted, the value threshold of the main contract seems to be difficult to break because of the rigid demand, as long as the price is low, the buyer It is possible to buy and deliver, but due to the distribution of the delivery warehouse and the quality of the oil, the price of the arbitrage anchorage of Shanghai crude oil futures is not very clear. First, the distribution library is too widely distributed. At present, Shanghai Energy 600508, the stock bar trading center announced six crude oil futures designated delivery warehouses, distributed from Dalian in the north to the coastal areas of Zhanjiang Port in the south, including Liaoning Dalian, Shandong Dongjiakou, Shandong Rizhao, Zhejiang Ningbo Daxie, Zhejiang Zhoushan, Eight reservoir areas of Shanghai Yangshan Port and Zhanjiang Port of Guangdong Province have a total storage capacity of 5.95 million cubic meters and a storage capacity of 3.15 million cubic meters. In addition, Dalian Port 601880, Share Bar Co., Ltd., Yingkou Port 600317, Shares Xianrendao Wharf Co., Ltd., and CNOOC Yantai Port Petrochemical Storage Co., Ltd. were also approved. The distribution of the WTI with the United States is different in the Cushing area, and the distribution of the Shanghai crude oil futures is very scattered. In addition, the Cushing area of ​​the United States is connected to a number of oil pipelines that can be quickly transported through pipelines to major refineries. The delivery warehouse of Shanghai crude oil futures is basically a limited refinery. As a buyer, if the decision is made to deliver, the location of the warehouse receipt delivery warehouse that is obtained cannot be satisfied, which will make it necessary to set aside more price space for the arbitrage calculation. From a prudent point of view, the buyer needs to pave himself a price of the Shanghai crude oil futures contract price and the bottom of the Oman crude oil into the tank cost difference at the time of the transaction. In the worst case scenario, the warehouse receipt will be delivered from the delivery. When the Kuti oil is transported to the designated spot warehouse for two-way transportation, the cost will be paid. Only when the spread can be covered will there be sufficient price safety margin and the buyer's determined arbitrage impulse. Therefore, the cost of the two-way sea transportation to Zhanjiang to all parts of the country needs to be mastered. If the domestic customers are going to deliver oil in the delivery warehouse, they need to rent a domestic tanker for the second-way transportation. It belongs to the domestic trade and ocean transportation. It is understood that Zhanjiang is The freight rate of domestic trade tankers in Huangdao, Shandong is 120 yuan / ton (2.6 US dollars / barrel). At the same time, the buyer also needs to bear the expenses for the storage and loading of oil, which need to be listed together in the calculation. 6 crude oil futures designated delivery warehouse storage information Unit: 10,000 cubic meters The general sales model of oil producing countries in the Middle East is two types, one is a long-term contract and the other is a spot. The price of the long-term contract is announced by the official national oil company monthly for the next month's crude oil pricing formula. In April 2015, Iraq divided the crude oil produced into two types, one was the original Basra light crude oil and the other was the Basra heavy crude oil. Iraq follows Saudi Arabia in oil pricing, especially the official price formula of Basra light crude oil, which maintains a strong correlation with Saudi medium crude oil. Since the benchmark crude oil is based on the monthly average price of Platts Dubai and Oman crude oil, the official price increase reflects the price difference between the oil and the benchmark crude oil Dubai and Oman crude oil in the Middle East. From the trend of official prices, the price difference between Basra Light Crude Oil and Dubai and Oman has been strong since January 2015. This has led to a significant reduction in the price advantage of Basra's light crude oil, considering that there is an API adjustment in Iraq for the actual delivery of crude oil (that is, based on 34, the actual oil extraction API is reduced by 0.4 US dollars per barrel per unit of the API). Basra light crude oil is still most likely as the worst quality delivery oil. The acquisition of Basra crude oil is much higher than that of Oman crude oil; national oil companies generally do not sell long-term contract crude oil to non-refiner background customers, which greatly restricts the freedom of access to resources, for industrial customers. A reserve of deliverable oil is added to the hand. It should be noted that there is no risk that the industrial customers will use the Basil light crude oil as the delivery of crude oil. The main risk is that the official price announcement of Basra light crude oil is inconsistent with the spot trading window of Dubai and Oman crude oil in the Middle East. The Middle East Oman crude oil futures adopt M+2 system, and the Dubai window trading also adopts M+2 system. Basra light crude oil The official price announcement is the M+1 system. It also means that at the time of M, the discount of the light crude oil of Basra, which was raised in M+2 months, was not known, so it was impossible to determine the exact discount of Basra light crude oil relative to Dubai and Oman crude oil. The formulation of the official price system of the entire Middle East crude oil is complicated, and the national oil companies will not fully disclose their official price setting models. Therefore, the introduction of Basra light crude oil as the delivery oil has increased the cross-regional arbitrage of Shanghai crude oil futures. Anchoring the complexity and interest of measurement. Figure 3 April 2015-2018 March Basra light crude oil and Arabian medium crude oil official price discount chart It is the volatility of cross-regional spreads that has really promoted cross-regional arbitrage trade and achieved price linkages of global benchmark crude oil. Therefore, the key is that as long as this arbitrage trade can be carried out without excessive import policies, unreasonable logistics conditions and variety conditions, under the cross-regional arbitrage price anchoring mechanism, normal fluctuations will be enough to make Shanghai crude oil futures International crude oil futures have a strong price linkage. 3. Two-stage intertemporal market of Shanghai crude oil futures: using inter-period structure for arbitrage Looking at the logic of the inter-temporal spread and the fundamentals, the forward price curve of the futures market has important fundamental significance. Under the near-low and high futures market price structure, the regional market's oversupply is reflected, while under the near-high and low structure, the supply exceeds demand. Research shows that the inter-temporary spread between WTI crude oil futures contracts in different months is related to US crude oil inventories, which also proves the effectiveness of the futures market for the balanced supply and demand of the market. Shanghai crude oil futures also need to be able to output such a curve in order to become a true barometer of regional market supply and demand. Outside the main contract, the individual believes that the forward curve can be divided into two segments. The first paragraph is the inter-period price structure between Shanghai crude oil futures from the first line (M+1) to the main contract (M+April). The second paragraph is the intertemporal price structure that has been formed after the main contract has been extended to longer-term contracts. When the price of the near-month contract is lower than the price of the main contract and exceeds the warehousing and capital cost of holding the warehouse receipt, it will trigger a positive inter-temporal arbitrage and encourage the accumulation of inventory; while the near-month contract price is higher than the main contract, it will lead to the reverse. Inter-arbitrage arbitrage, stock drop was released. In the regional market, inventory will play a mobile “demand†and “supplyâ€, which will cushion the short-term supply and demand balance in the region. Therefore, the rationality of the market's inter-period spread will also test the ability of Shanghai crude oil futures to reflect the balance of supply and demand in the region. Personally, the first inter-period spread is expected to become a local barometer of the balance between supply and demand of China's imported medium-grade sulfur crude oil. The second inter-period spread will be more replicated according to the structure of the international crude oil market, and individuals may think that it may be close to the Brent crude oil futures or the market structure of Dubai's long-term. The reason why Shanghai crude oil futures will form a two-stage intertemporal structure is related to the futures contract month rule. The first contract month of Shanghai crude oil futures is closer to WTI crude oil futures, all of which are M+1. That is, the first contract for the mid-March trade was in April. The April WTI contract delivery can be carried out in April, and the Shanghai crude oil futures contract delivery in April is the first 5 working days in April (the 5th delivery method). The difference is that US domestic crude oil plus Canadian crude oil supply to the United States currently accounts for 70% of the share, while China imports 70% of imported crude oil. Therefore, the first line of US WTI crude oil futures can be based on the local market for pricing. The first contract is the main contract; the first contract of China Shanghai crude oil futures cannot be priced according to the local market supply, and it needs to import crude oil from a longer period. The price of the main contract to be anchored is reversed. The first inter-period spread, including the first row, the second row, the third row, and the main contract. The price structure will reflect the holding value of the warehouse receipts and local spot demand. The warehouse receipt can be pledged, so the cost of holding the warehouse receipt is not high. The main problem is the warehousing cost. The current price is 0.2 yuan / barrel day, and the monthly storage cost is 6 yuan / barrel, which is higher than the current floating warehouse cost and the storage cost in the Cushing area of ​​the United States. If you want to encourage the holding of warehouse receipts, it obviously needs a monthly structure of nearly 1 US dollar / barrel. In theory, if the refinery lacks interest, it means that the price of the first line will be lower than the main contract by nearly 3 US dollars / barrel. The second inter-period spread, including the extended contract from the main contract. Since there is currently no market maker, the effectiveness of liquidity and spreads is indeed worrying. Just as the main contract has inter-temporal arbitrage anchoring, the month farther than the main contract, and the long-term counterparty of Dubai and Oman in the Middle East also have similar cross-regional arbitrage mechanism. Therefore, the formation of the second inter-period spread can refer to Dubai. The long-term structure and monthly difference between Oman crude oil and Oman. At this stage, the overall forward curve structure of WTI and Brent crude oil futures in the international crude oil market is near high and low, and there may be interesting phenomena in the initial stage of Shanghai crude oil futures, that is, the first segment is near low and high and second. The near-high and low combination of the segment. On March 12, Shanghai crude oil futures announced that the first contract of the listed transaction was 1809 contract. According to the main contract month if it really appears in M+4 (Note: M+3 is also possible), starting in May, the trading liquidity of the 1809 contract will gradually decrease, and the position will also decrease, while the 1810 contract Trading liquidity and positions will increase, and the June 1810 contract officially replaced the 1809 contract as the main contract. The monthly difference between the two is worthy of close attention by traders and falsification of the author's point of view. Once the price of the main contract is anchored by the cross-regional arbitrage mechanism, in the future, the first phase of the Shanghai crude oil futures contract will help to promote the spot market of medium-sized sulfur-containing crude oil in China and the Far East. At the same time, it will also promote the refinery's transformation of the crude oil procurement model in the Middle East, providing refineries with opportunities for resource optimization outside of regular long-term contracts and forward spot transactions. From this point of view, if there is a "delivery war" in the early stage of Shanghai crude oil futures, it is also a new starting point for the construction of China Petroleum 601857. This article was first published on the WeChat public account: Yi Dejing Yinghui. The content of the article belongs to the author's personal opinion and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk. (Editor: Chen Hao HF072) Roller Blind Curtain Shade Plain Dyed Fabric

100% polyester fabric, light and thin, good wear resistance, and good air permeability. Fabric include semi-blind and blind. Blind fabric's back coated with white or the color same with fabric. Many configuration options blackout, waterproof, protect UV according to the weather and your mood adjust brightness of the sun light

Fabric Roller Shades,Waterproof Blackout Roller Blinds,Waterproof Roller Blinds,Waterproof Blinds For Bathroom Window,Shade Plain Dyed Fabric SHAOXING JEVA IMP.&EXP CO., LTD. , https://www.xhcurtain.com

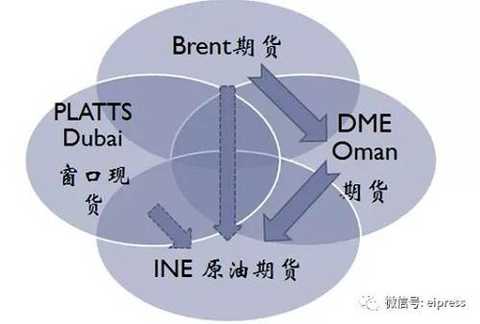

Among the three major crude oil futures, from the perspective of distance, the physical resources corresponding to WTI and Brent crude oil futures will arrive in China far more than the actual delivery of Oman crude oil futures; from the quality of oil, WTI and Brent crude oil and Oman The quality of crude oil varies widely. Therefore, in the cross-regional arbitrage, it is obvious that it is not necessary to be close to the distance, and the Shanghai crude oil futures price is correlated with WTI and Brent. Oman crude oil is one of the deliverable oils of Shanghai crude oil futures. Oman crude oil is currently the easiest and most straightforward cross-regional arbitrage price anchoring oil. Oman crude oil has futures trading, namely DME Oman crude oil futures. The transaction is open and transparent, and it can be physically delivered to obtain standard Oman crude oil.

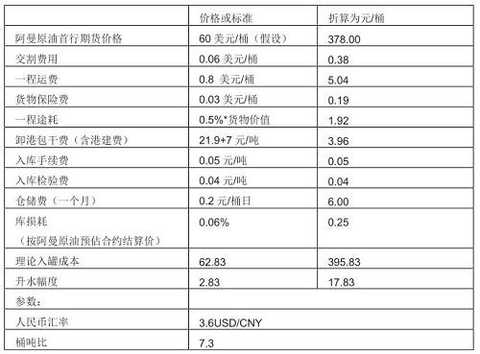

Second, the main contract operates on a cross-regional arbitrage mechanism to achieve reasonable fluctuations in cross-regional spreads. The important fundamental role of cross-regional arbitrage is to link the prices of crude oil in the two regions. From the arbitrage point of view, if the M+2 month Oman crude oil futures plus miscellaneous charges (to the shore into the tank) is lower than the M+4 Shanghai crude oil futures, you can buy INE crude oil futures by buying Oman for arbitrage, arbitrage trading. The next feedback will pull the high Shanghai crude oil futures price back to the normal range of fluctuations.

The second thing to note is the diversification of the delivery oil, and the existence of bad money to drive out the good money effect. Among the four crude oils of BFOE in Beihai, the crude oil quality of Forties is the worst, so the so-called Brent crude oil spot is basically based on the price of Forties crude oil. Among the six countries in Shanghai crude oil futures, the Masai crude oil in Yemen is +5 yuan / barrel of water, and the Iraqi Basra light crude oil has a subsidy of -5 yuan / barrel. Masila crude oil resources are small, and Yemen’s current situation is turbulent, so it is not the focus of consideration in a short time. Basra's light crude oil clearly needs to be given high attention. Since the quality of Basra's light crude oil is significantly worse than that of Oman and Abuzhacom crude oil, it is set as a discount when it is used as a delivery oil. Therefore, Basra is likely to become a "bad currency" in the delivery of Shanghai crude oil futures.

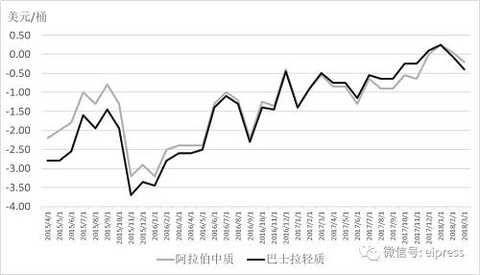

Although the cross-regional arbitrage anchoring is clear in principle, due to the setting of the delivery warehouse and the diversity of oil types, the fluctuation of the spread will definitely be brought about. However, with reference to the volatility of the spread between WTI and Brent crude and Brent crude and Dubai crude, we can see that the fluctuations in the spread of Brent crude oil and WTI crude oil have been huge and dramatic in the past five years; The fluctuations in the spread of Brent and Dubai and Oman crude oil also fluctuated between 0-5 USD/barrel.